")

A Guide to Balance Sheets and Income Statements

By: Michael Jones

When you own a small business, organization and good recordkeeping are two of the most powerful tools you have at your disposal. Keeping track of things like sales, outstanding invoices and monthly expenses is essential to understanding how healthy your business is at any given moment.

Proper records are also a must if you plan to seek a business loan or another form of small business financing. Before your loan can be approved, the lender will need documentation showing how financially sound the business is. That’s where a balance sheet and income statement come into play.

These two documents play an important role in the loan application process and without them, you may find it difficult to get the financing your business needs. If you’re confused about what these documents are or how to get started with creating them, this guide is designed with you in mind. By the time you’ve finished reading, you’ll understand:

- What a balance sheet and income statement are

- How to create your initial balance sheet and income statement

- How to maintain these documents going forward

- Why these documents are used in loan applications

Financial Documents 101

The first step in getting your small business’s financial house in order is knowing what balance sheet and income statement are and what they’re not. Though the two appear similar, they each serve a very different purpose.

What is a balance sheet?

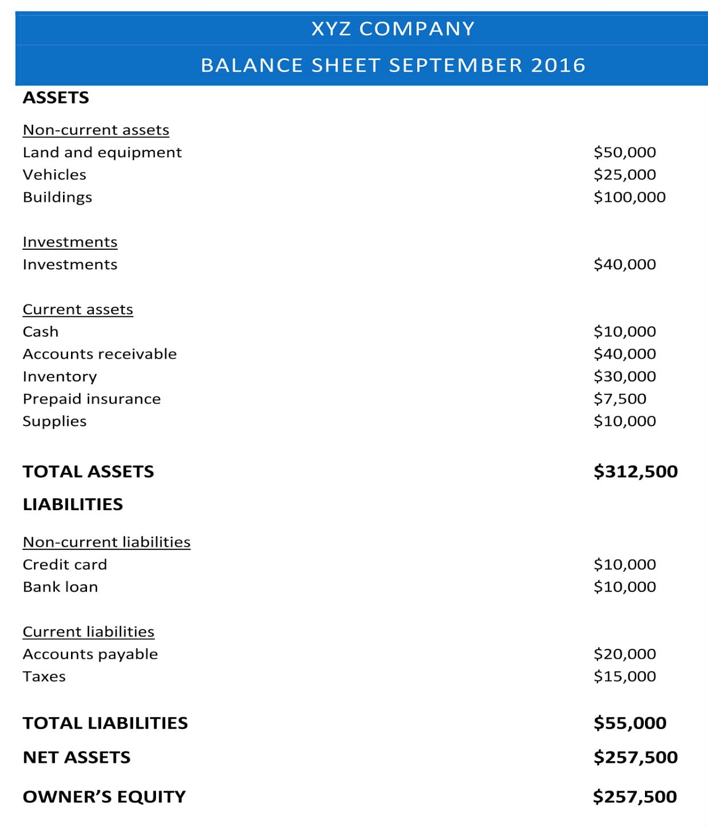

To put it simply, a balance sheet is a financial snapshot of your business at a specific point in time. For example, you may put together a balance sheet at the end of the fiscal quarter to get an idea of what your starting point is going into the next quarter.

A balance sheet, sometimes referred to as a statement of financial position, focuses on three distinct aspects of your business:

- Assets

- Liabilities

- Equity

Assets are things your business owns, such as equipment, inventory, accounts receivable or cash. Assets have a measurable value and they can be broken down on the balance sheet by category. For example, you can choose to sort them based on whether they’re current assets, investments owned by the business, real property, or intangible assets, such as a trademark or copyright.

Liabilities are any monies owed by the business. Liabilities may be short-term or long-term, depending on how they’re classified on the balance sheet. Accounts payable, outstanding payroll, and taxes could all fall under the heading of short-term liabilities. A long-term liability would be something that you’re making payments against over time, such as a business loan or credit card balance.

Owner’s equity is the third piece of the puzzle. This is what you as the owner are able to claim ownership of, once any liabilities are deducted from the business’s assets. Below is an example of what a completed balance sheet may look like:

Income statement basics

An income statement, also known as a profit and loss statement, shows how profitable your business was over the course of a specific accounting period. Think of it this way. The balance sheet tells you what your business’s assets and liabilities are, while the income statement tells you how your business used them.

Creating an income statement requires some basic math. The formula looks like this:

Revenue – Expenses = Net profit/loss

If there’s a surplus after you complete the calculation, this is your net profit. If you get a negative number, this is your business’s net loss.

Revenue refers to money that’s payable from the sale of goods and services, as well as interest received for a loan that the business has made to someone else, or gains earned in connection with the sale of a business asset.

Depending on how your business is structured and what your overhead costs are, your expenses may include any or all of the following:

- Rent or lease payments

- Utilities

- Supplies

- Employee wages and benefits

- Insurance

- Taxes

- Advertising costs

- Travel expenses

One crucial thing to be aware of when drafting an income statement is the difference between revenues and receipts. Revenue is the money your business has earned during the reporting period. Receipts are when the money is actually paid to you.

When you’re formulating an income statement, you need to be able to distinguish revenues from receipts clearly so that you don’t end up reporting them twice. This could cause your net income to look inflated on paper and result in an inaccurate picture of how profitable the business is.

Documents other than balance sheets and income statements

While a balance sheet and income statement are two central pieces of information you’ll need to measure the financial soundness of your business, there are other records you should be keeping as well.

A cash flow statement, for example, breaks down how much money is coming and going out of the business. To create a cash flow statement, you add your cash inflows to your beginning cash balance, then subtract your outflows.

Along with your balance sheet and income statement, the cash flow statement is necessary to complete your quarterly and annual tax filing. If you’re not clear about how much money your business is making or what you’re paying out in expenses, you may miss valuable deductions or risk underpaying your estimated taxes.

How to Create Your Balance Sheet and Income Statements

If you’ve never completed a balance sheet for your business before, getting started isn’t as difficult as you might think. It all comes down to three key steps.

- Add up all of your business assets. We’ve explained what constitutes an asset earlier but if you need a refresher, that means things like cash, securities, accounts receivable, inventory, land, equipment, intellectual property, supplies and any insurance for the business that you’ve prepaid.

- Calculate your business liabilities. On the liabilities side, you’d list accounts payable, taxes owed, unearned revenue, bonds payable, wages, payroll and any loans or lines of credit the business is responsible for.

- Determine the value of your equity. Once you’ve tallied up all of your assets and all of your liabilities, you can move onto the final step. Subtract your liabilities from your assets to come up with your equity figure.

How you actually draw up a balance sheet depends entirely on your preference. You could do it the old fashioned way with pen and paper but creating a simple spreadsheet can make the process easier. If you’re not a spreadsheet wizard, below is a downloadable form that you can use as a jumping off point:

Once you’ve got your balance sheet in order, you can move on to creating your income statement. The steps are a little different but the process isn’t complicated. Here’s what you need to do:

- Choose a time frame. Income statements can cover a shorter time period or a longer one, depending on what you’re planning to use it for. Before you start crunching numbers, decide if you’re going to look at your business’s profitability from a monthly, quarterly, biannual or annual perspective.

- Add up all of your business income. Again, the most important thing to remember is not to confuse your revenues with your receipts for the time period in question.

- Subtract expenses from revenues to get your profit or loss. When you’re calculating expenses, make sure you’re including any and everything you spend to keep the business up and running. That includes the big things like payroll and taxes, as well as smaller expenses like monthly web hosting or printing fees for business cards.

Just like your balance sheet, you can create an income statement on paper or in a spreadsheet form.

Maintaining Your Balance Sheet and Income Statement

Setting up your balance sheet and income statement for the first time may take a little work but it becomes easier to keep up with these documents after getting over that initial hurdle. The trick is to make maintaining them a priority without having to invest hours of your time.

So how do you do that? Start by scheduling a regular time to review your balance sheet and income statement. Whether you choose to do it once a month or once a year is up to you but the key is to be consistent about when you do it.

Next, consider utilizing a good accounting software if you’re not doing so already to keep tabs on your receivables, accounts payable, monthly expenses, equipment purchases, tax payments, payroll and so on. If you’ve got all of this information organized in an easily accessible format, all you’ll need to do to complete your balance sheet and income statement is plug in the numbers.

How a balance sheet and income statement can help your business

Incorporating a balance sheet and income statement into your recordkeeping system benefits your business on several levels but it’s not a once-and-done proposition. Updating these documents on an ongoing basis can benefit your business on several levels.

The balance sheet allows you to see at a glance what your financial status is. If you have negative equity in the business, for instance, that’s a sign that you’re either don’t have enough assets or you’re carrying too much debt. Without a balance sheet as a reference, you could be sinking your business financially without even realizing it. Aside from that, it’s helpful to be able to see how your assets and liabilities have increased or decreased over time.

The income statement is just as important because it shows you how your spending compares to what you’re bringing in. When your net profit is smaller than you anticipated or you’re ending each month in the red, that can be a motivator to look for ways to bump up your revenues and cut your expenses to get back in the black. It also makes it easier to spot trends, such as which months see a spike in revenue and which ones leave you with a smaller cash flow.

Why Bond Street Requires These Documents for Our Loans

As a provider of term business loans, Bond Street requires applicants to complete a thorough underwriting process before being approved. When you complete an application with us, we’re want to see how your business is doing in terms of revenue but we’re especially interested in the bottom-line view with regard to profitability.

Your balance sheet and income statement paint a more complete financial picture than what we can see based just on your tax records or credit score alone. These documents are indication of how effectively you’re managing your small business and how strong your financial position is. That in turn, allows us to gauge the degree of risk that’s involved in lending.

As a rule, we require a minimum of two years’ worth of income statements as well as an up-to-date balance sheet to apply. If you don’t have these records on file but you’re interested in applying for a term loan with Bond Street, now’s the time to put the tips we’ve outlined here to work.

Trending Articles